Related Categories

Related Articles

Articles

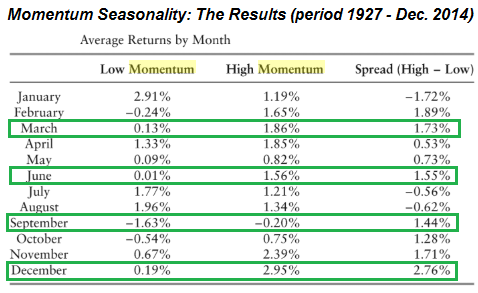

Quantitative Momentum (Quarter-ending months)

RECHECKING

"Quantitative Momentum: A Practitioner's Guide to Building a Momentum-Based..."

(Authors: Wesley R. Gray, Jack R. Vogel)

Quarter-ending months generally have the highest returns when comparing low and high momentum portfolios. Once momentum-profits are...

...the largest in quarter-ending months, and this is likey driven by managers who are window dressing their portfolios, one might hypthesise that rebalacning before these quarter-ending months will yield the hightest returns...